Limited Companies for UK Property Investment: What Actually Matters

Thesis

The surge in limited company property ownership across the UK private rented sector is often framed as a simple tax optimisation story. That interpretation is incomplete — and for many investors, actively misleading.

Hamptons' analysis of Companies House records reported 345,426 active limited companies designed to hold buy-to-let property at the start of 2024, with 68% of those companies having been set up between 2017 and 2023. This points to a major structural shift in how UK residential property is being owned and managed. The acceleration coincided with the rollout of Section 24 of the Finance Act 2015, which materially altered the economics of leveraged personal ownership.

In reality, the limited company decision is a structural portfolio decision — one that interacts with financing constraints, taxation mechanics, operational complexity, and long-term exit planning. It determines how capital flows through a property portfolio: how profits are retained, how leverage is serviced, how refinancing is underwritten, and how exits are taxed.

For some investors, companies provide a framework for capital discipline, refinancing flexibility, and portfolio scalability. They enable retained earnings to compound within the structure, simplify multi-property lending arrangements, and impose the kind of operational rigour that larger portfolios demand.

For others, they introduce unnecessary administrative friction, trapped profits, and new tax complications that outweigh the benefits. A two-property landlord with low leverage and an income extraction requirement may find that a company structure adds cost and complexity without improving returns.

Limited companies do not eliminate tax for property investors; they change the timing and location of taxation within the investment lifecycle.

The critical question is therefore not:

"Is a limited company more tax efficient?"

The real question is:

What ownership structure best supports the investor's capital strategy, financing model, and long-term exit plan?

This article examines the structural drivers behind the shift toward company ownership — and the situations where it genuinely improves investor outcomes.

For many landlords the limited company debate is framed incorrectly. It is rarely about tax optimisation alone. It is about how property portfolios behave under leverage, refinancing cycles, and long-term capital compounding.

Key Takeaways

Key takeaways for property investors

The Structural Shift Toward Corporate Ownership

The debate around limited company ownership is not occurring in isolation. Over the past decade the structure of UK buy-to-let ownership has changed materially.

Following the introduction of the Section 24 mortgage interest restriction under the Finance Act 2015, a growing share of new property acquisitions began taking place through corporate vehicles rather than individual ownership.

Industry and broker research indicates that a growing share of new buy-to-let purchases are now made through limited companies, typically structured as Special Purpose Vehicles (SPVs) created specifically for property investment. Many specialist lenders prefer straightforward property-holding SPVs and often look for property-related SIC codes such as 68100 (Buying and selling of own real estate) or 68209 (Other letting and operating of own or leased real estate), although exact criteria vary by lender.

This shift reflects a broader structural transition within the private rented sector. Historically, the UK rental market was dominated by small individual landlords holding one or two properties. Increasingly, however, portfolio investors are operating their holdings through formal corporate structures.

Several factors are contributing to this change:

- the tax treatment of mortgage interest

- rising refinancing complexity

- greater regulatory oversight

- increasing professionalisation of landlord operations

For investors building multi-property portfolios, the ownership structure has therefore become a strategic component of portfolio design rather than merely a tax consideration.

Why Limited Companies Surged in Popularity

The growth of company ownership in UK residential property accelerated sharply after 2017. Hamptons' analysis of Companies House records reported 50,004 new limited companies designed to hold buy-to-let property in 2023 alone, taking the total number of active such companies to 345,426 at the start of 2024.

The structural catalyst was Section 24 of the Finance Act 2015 — formally the restriction on finance cost relief for individual landlords — which phased in between the 2017–18 and 2020–21 tax years. Under HMRC's current rules, individual landlords can no longer deduct all residential finance costs directly from rental income when calculating taxable property profits. Instead, relief is given through a basic-rate tax reduction equal to 20% of the relevant finance costs, subject to HMRC's calculation rules.

For higher-rate (40%) and additional-rate (45%) taxpayers, the result is often taxation on gross income rather than true economic profit. In extreme cases — particularly where loan-to-value ratios are high and mortgage payments consume a large share of rental income — landlords can face tax liabilities that exceed their actual cash surplus.

| Scenario | Personal Ownership | Company Ownership |

|---|---|---|

| Rental income | £20,000 | £20,000 |

| Mortgage interest | £12,000 | £12,000 |

| Taxable income | £20,000 | £8,000 |

| Tax at 40% | £8,000 (less 20% credit: £5,600 net) | N/A |

| Tax at 25% corp | N/A | £2,000 |

Under personal ownership, the landlord in this example pays £5,600 in tax on £8,000 of economic profit — an effective rate of 70% on actual cashflow. Under company ownership, the same economic profit attracts £2,000 in corporation tax. The difference is not marginal; it can determine whether a leveraged portfolio remains viable.

This structural change pushed many leveraged landlords toward corporate ownership. But the tax driver alone does not explain the full trend.

Other forces are also shaping investor behaviour:

- Refinancing pressure across the sector, as fixed-rate periods expire and portfolios face repricing at higher interest rates

- Increasing portfolio scale among professional landlords, with the PRA's portfolio landlord classification (four or more mortgaged buy-to-let properties) triggering enhanced lender underwriting

- Institutionalisation of the private rented sector (PRS), with larger operators adopting corporate governance structures

- Professionalisation of landlord operations, driven by expanding regulatory obligations under the Renters' Rights Bill and energy performance requirements

These forces were explored in PropMatch's analysis of the UK refinancing cycle. Read our guide on UK Buy-to-Let Refinancing Wave: Structural Risk Investors Are Underestimating to understand how refinancing pressure shapes ownership decisions.

Ownership structure increasingly affects how investors navigate refinancing risk — and the decision to incorporate is frequently made in the context of a refinancing event rather than as an abstract tax planning exercise.

The Tax Mechanics Investors Actually Misunderstand

Many discussions around property companies reduce the issue to a simplistic claim:

"Companies are more tax efficient."

That claim is often misleading because it conflates the tax rate on retained profits with the total tax burden across the investment lifecycle.

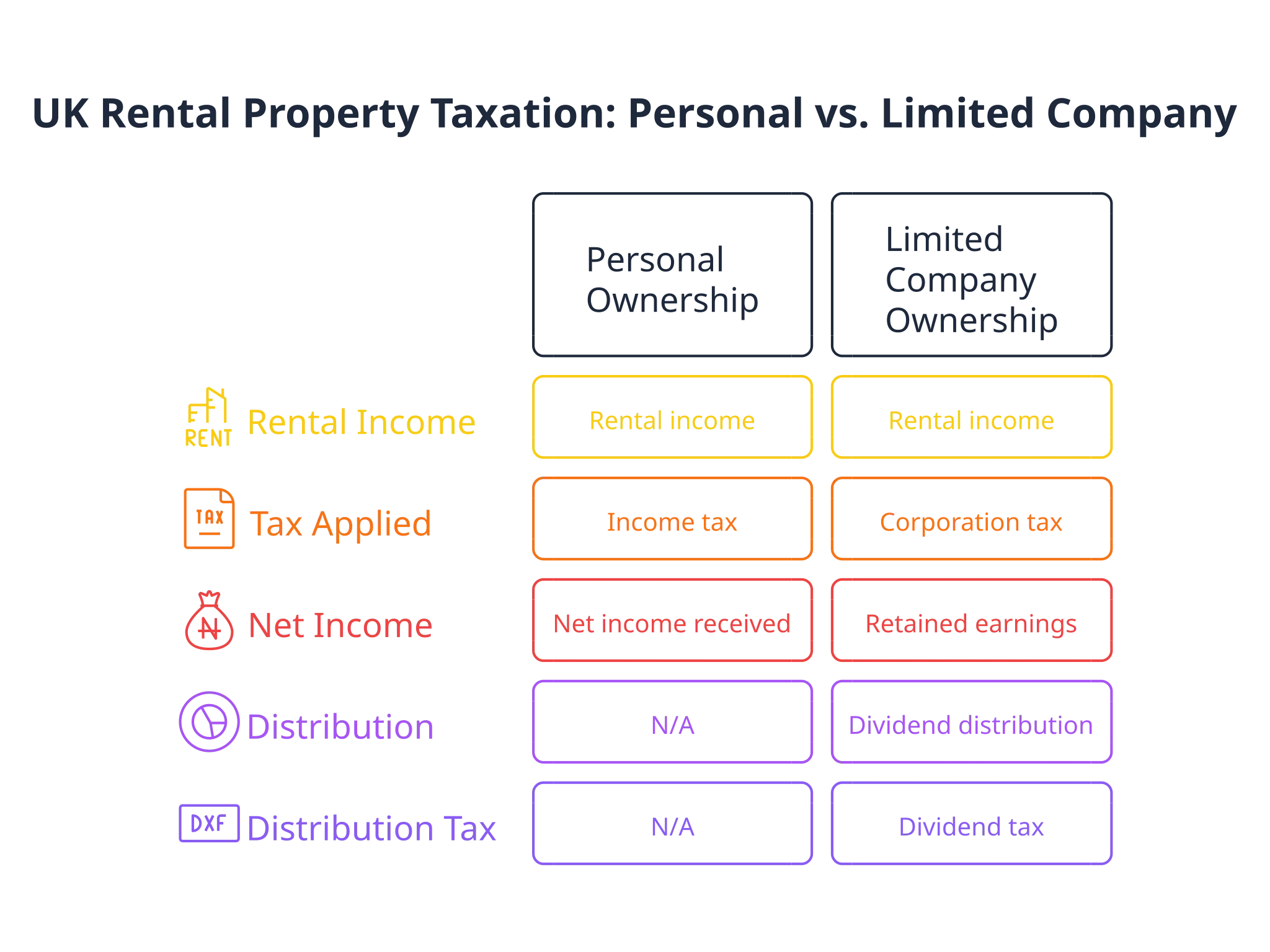

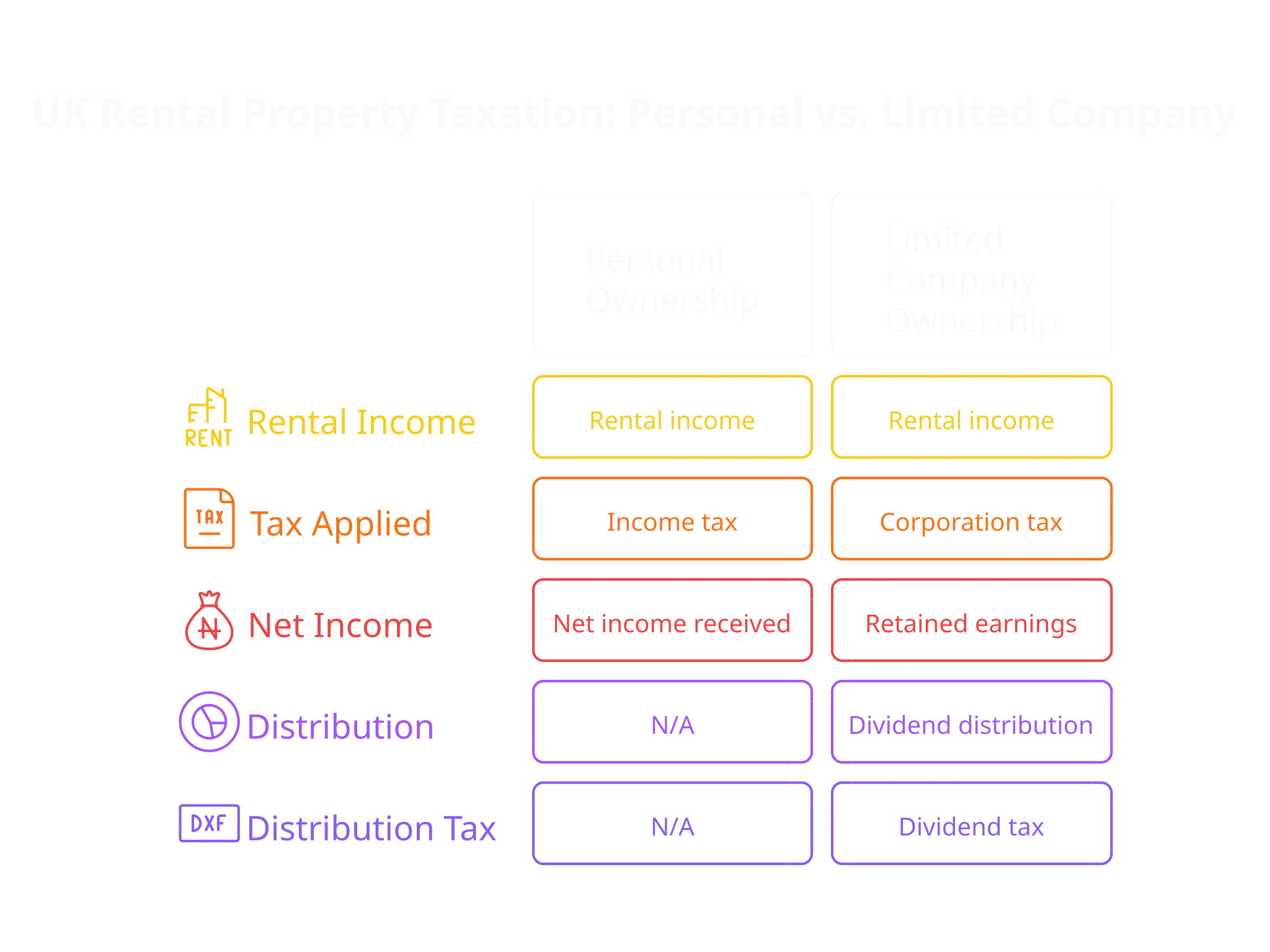

Companies do not eliminate tax. They restructure the sequence and incidence of taxation — deferring some liabilities while introducing others that do not exist under personal ownership.

Personal ownership

Under personal ownership, tax occurs immediately as income is received:

- Rental income is taxed at the investor's marginal income tax rate (20%, 40%, or 45% depending on total income).

- Residential finance costs are restricted under Section 24 — relief is generally given through a 20% tax reduction rather than full deduction.

- As at the 2025–26 tax year, Capital Gains Tax is payable on residential property gains at 18% within the basic-rate band and 24% above it, after the annual exempt amount where available.

The advantage of personal ownership is simplicity: there is a single layer of taxation and no extraction friction. Profits flow directly to the individual.

Company ownership

Corporate structures introduce two distinct layers of taxation, and the total burden depends on what the investor does with the profits:

- Corporation tax on company profits — as at 2025–26, 25% for companies with profits above £250,000, with a small profits rate of 19% for profits of £50,000 or less and marginal relief between those thresholds.

- Dividend tax when profits are extracted — as at 2025–26, 8.75% (basic rate), 33.75% (higher rate), or 39.35% (additional rate), after the £500 annual dividend allowance.

How tax occurs under personal vs corporate property ownership

| Tax Stage | Personal | Company |

|---|---|---|

| Rental profit | Income tax (up to 45%) | Corporation tax (19–25%) |

| Profit extraction | None | Dividend tax (8.75–39.35%) |

| Property sale | Capital gains tax (18–24%) | Corporation tax on gain + potential dividend tax |

This can be advantageous if profits are reinvested — for example, used as deposits for further acquisitions, or retained to build reserves against void periods and maintenance liabilities. Within the company, profits compound at the post-corporation-tax rate without triggering additional tax until they are distributed.

It is less beneficial if the investor needs income today. A higher-rate taxpayer who extracts all company profits as dividends faces a combined effective tax rate (corporation tax plus dividend tax) that can approach or exceed the marginal income tax rate under personal ownership — particularly once the administrative cost of maintaining the company is factored in.

For a deeper examination of capital gains mechanics and tax planning, see our Capital Gains Tax on Property article.

To model the tax impact of different ownership structures, use our Budget 2025 Tax Calculator to assess personal and company ownership scenarios.

Common Misconceptions About Property Companies

The rapid increase in corporate ownership has produced a number of simplified narratives in investor forums and property media. Many of these narratives obscure the actual trade-offs involved in the decision.

One common misconception is that limited companies are inherently more tax efficient than personal ownership. In reality, corporate structures do not eliminate taxation. They change the point at which taxation occurs, shifting part of the tax burden from income to profit extraction or eventual disposal.

Another misconception is that existing property portfolios should automatically be transferred into a company. In many cases, transferring personally owned property into a corporate structure triggers both Stamp Duty Land Tax and Capital Gains Tax, which can make the restructuring economically unviable unless the portfolio is large or held within a qualifying partnership structure.

A third misconception is that companies eliminate capital gains tax entirely. While companies pay corporation tax on gains rather than capital gains tax, the investor may still face further taxation when proceeds are distributed as dividends.

Understanding these distinctions is critical. The ownership structure decision is not about avoiding tax altogether but about how tax interacts with leverage, reinvestment strategy, and long-term capital allocation.

The Real Decision: Portfolio Structure vs Tax Optimisation

The limited company decision is often framed incorrectly. It is rarely just about tax. Instead, it reflects how the investor intends to operate, finance, and eventually exit their portfolio.

Three investor archetypes illustrate the distinction.

Income investors

Characteristics:

- Small portfolios (typically one to three properties)

- Low leverage (below 50% LTV or mortgage-free)

- Income extraction as the primary objective

For these investors, personal ownership can remain efficient. Section 24's impact is modest when finance costs are low relative to rental income. The administrative complexity and annual costs of a limited company can represent a meaningful drag on net returns from a small portfolio. For an investor with £10,000 in net rental profit, even £1,500 in annual compliance costs would represent a 15% reduction in returns before any tax advantage is considered.

Portfolio builders

Characteristics:

- High leverage (65–75% LTV across the portfolio)

- Ongoing acquisitions funded by refinancing and retained earnings

- Refinancing as the primary capital recycling mechanism

For this group, companies often improve cashflow materially because full interest deductibility is restored. Retained profits accumulate within the structure at the corporation tax rate, providing equity for further acquisitions without triggering dividend tax. Consider an investor generating £40,000 in annual pre-tax profit across a leveraged portfolio: under personal ownership at 40% marginal rate with Section 24 restriction, the after-tax position may leave insufficient capital for deposits on further purchases. Inside a company, the same profit retains £30,000–£32,400 (depending on the applicable corporation tax rate), which can be deployed immediately.

Long-term capital allocators

Characteristics:

- Multi-property portfolios (ten or more units)

- Professional management arrangements

- Long holding periods with no near-term exit requirement

Here the structure becomes part of capital discipline rather than tax minimisation. The company imposes governance — filed accounts, documented director decisions, clear separation between personal and portfolio finances. For investors whose portfolios have reached a scale where informal record-keeping creates risk, the corporate wrapper provides a framework that supports both operational management and eventual succession planning. The limited company structure, at scale, functions less as a tax vehicle and more as an institutional governance framework for private capital.

When Limited Companies Genuinely Make Sense

Corporate ownership tends to be advantageous under specific, identifiable conditions.

Highly leveraged portfolios

Mortgage interest deductibility becomes extremely valuable when finance costs represent 50% or more of gross rental income. The difference between paying tax on gross rent (personal ownership under Section 24) and paying tax on net profit (company ownership) can determine whether a portfolio generates positive cashflow or operates at a loss on an after-tax basis. For investors refinancing at rates above 5%, this distinction is increasingly material.

Investors reinvesting profits

If profits remain inside the company, dividend tax can be deferred indefinitely. Capital compounds within the structure at the post-corporation-tax rate. Over a ten-year horizon, the compounding advantage of retaining 75–81% of profits (versus extracting and paying combined rates that may retain only 55–65%) can be substantial — particularly if retained capital is deployed into further acquisitions that generate their own returns.

Portfolio scaling

Companies facilitate multiple property acquisitions within a single legal entity, or across a group of related SPVs. They provide clearer accounting separation between properties, simplify structures where multiple investors co-own portfolios, and can make ownership changes or succession planning operationally cleaner — although the tax outcome depends heavily on how the structure is set up and how any exit is executed.

Professionalisation of operations

Larger portfolios increasingly resemble operating businesses. Companies House obligations — annual confirmation statements, filed accounts, maintenance of the persons with significant control (PSC) register — impose a discipline that is broadly aligned with the operational requirements of managing a substantial property portfolio. For investors employing managing agents, maintaining insurance programmes, and operating structured maintenance schedules, the company framework mirrors the operational reality.

When Companies Introduce Unnecessary Complexity

Corporate ownership is not universally beneficial. In many cases, the disadvantages outweigh the gains, and investors would achieve better net returns through personal ownership.

Low leverage portfolios

If mortgage costs are small relative to rental income, Section 24 has limited practical impact on after-tax returns. An investor with 30% LTV across a portfolio may find that the restricted interest relief produces a tax liability only marginally higher than under the old rules. The incremental tax saving from incorporation would not cover the annual compliance costs.

Investors needing regular income

Dividend taxation creates extraction friction that reduces the net benefit of corporate structures. A higher-rate taxpayer who extracts all company profits as dividends faces a combined corporation tax and dividend tax burden that can closely approximate the personal income tax rate — typically producing a combined effective rate of approximately 46–54% depending on the applicable corporation tax rate. The company structure is advantageous primarily for capital accumulation, not income distribution.

Small portfolios

Administrative costs for a property company include annual accountancy fees, Companies House filing fees, corporation tax return preparation, bookkeeping support, and potentially registered office services. For a small portfolio, these costs can represent a material percentage of net profit. For a larger portfolio, they are proportionally less significant and may be outweighed by the tax and structural advantages.

Existing personal portfolios

In many cases, transferring property from personal ownership into a company is treated as a disposal at market value for CGT purposes, and the acquiring company may also face SDLT on the acquisition value. Reliefs may exist in some qualifying business or partnership scenarios, but these are highly technical and should be verified before any restructuring is assumed to work. For a property with significant embedded gains and no offsetting losses, the combined tax cost can still run to tens of thousands of pounds, making retrospective restructuring economically unviable in many cases.

Refinancing and Lender Behaviour

Financing dynamics increasingly shape the ownership decision, and for portfolio landlords in particular, lender underwriting behaviour may be a more immediate driver than taxation.

Buy-to-let lenders regulated by the FCA (or operating under the exemptions available for business-purpose lending) often treat corporate borrowers differently from individuals.

| Feature | Personal | Company |

|---|---|---|

| Mortgage rates | Often lower in straightforward cases | May be higher, depending on lender and structure |

| Portfolio structures | Can become more complex above 4 mortgaged properties | Often administratively cleaner for multi-property portfolios |

| Underwriting | Personal income and existing commitments often feature more heavily | Portfolio cashflow and rental coverage often carry more weight |

| Stress testing | Affordability and background income may feature | ICR (interest coverage ratio) and portfolio metrics are often central |

Common lender requirements include:

- Specific SIC codes registered with Companies House

- No trading activities beyond property ownership and letting

- Ring-fenced property assets with no unrelated liabilities

- Personal guarantees from directors

UK Finance data indicates that limited company buy-to-let lending has grown as a proportion of total buy-to-let origination over the past five years, reflecting both the Section 24 incentive and the development of specialist lending infrastructure. For portfolio landlords — those holding four or more mortgaged buy-to-let properties, per the PRA's classification — lenders are expected to use a specialist underwriting process. That can make company structures operationally cleaner for some larger borrowers, although it does not mean company borrowing is automatically cheaper or easier in every case.

However, for smaller investors with one or two properties, the rate premium on company lending and the additional administrative requirements may outweigh any underwriting benefit.

Operational Complexity and Professionalisation

Owning property through a company transforms the operational model. Landlords become directors of a property operating entity, subject to the Companies Act 2006 and the ongoing filing requirements administered by Companies House.

Responsibilities expand to include:

- Preparation and filing of annual statutory accounts (micro-entity, small company, or full accounts depending on thresholds)

- Annual confirmation statement to Companies House

- Corporation tax return (CT600) filed with HMRC

- Maintenance of the PSC (persons with significant control) register

- Structured bookkeeping separating company transactions from personal finances

- Dividend documentation, including board minutes for each distribution

For investors scaling portfolios, this professionalisation can be beneficial — it imposes the financial discipline and record-keeping that larger operations require. The company structure forces a separation between personal and portfolio finances that many individual landlords fail to maintain, and this separation can improve both tax compliance and investment decision-making.

However, many landlords underestimate the administrative burden, particularly the requirement to file accounts and returns on time (with penalties for late filing) and the public disclosure obligations that accompany corporate status. Certain company filings, including confirmation statements and filed accounts, are publicly accessible through Companies House, although the amount of financial detail available varies by company size and filing basis.

As explored in PropMatch's analysis of common investor errors, operational complexity is a recurring source of underperformance. Read our guide on Property Investment Pitfalls: Average Assumptions Failing UK Investors to understand how operational issues impact portfolio performance.

Operational complexity is a recurring source of underperformance — not because the requirements are onerous in absolute terms, but because they are frequently unanticipated and unbudgeted.

Exit Implications Investors Often Ignore

The tax treatment of exits differs materially between structures, and the exit pathway should be considered at the point of incorporation — not deferred until a sale is contemplated.

Personal ownership exit

Sale triggers Capital Gains Tax at the individual's applicable rate. As at the 2025–26 tax year, residential property gains are taxed at 18% within the basic-rate band and 24% above it. The annual CGT exempt amount (£3,000 for 2025–26) provides marginal relief. For an investor selling a property with a £100,000 gain, with the full taxable gain falling above the basic-rate band, the CGT liability at 24% would be approximately £23,280 after the exempt amount.

Company ownership exit

A property sale within the company triggers corporation tax on the gain at the prevailing rate (19–25%). The post-tax proceeds remain within the company. If the investor then wishes to extract those proceeds personally, a further layer of dividend tax applies.

For the same £100,000 gain, a company paying corporation tax at 25% would pay approximately £25,000 in corporation tax and retain £75,000. If a higher-rate taxpayer then extracted the full £75,000 as a dividend, and that distribution fell entirely within the higher-rate dividend band with the annual dividend allowance already used elsewhere, the dividend tax would be approximately £25,313. That would produce a combined tax burden of about £50,313 versus £23,280 under personal ownership. Different allowance and rate-band assumptions would change the precise number, but the broader point remains: a company exit can introduce a second tax layer on extraction.

Some investors mitigate this through:

- Retaining capital within the company and reinvesting proceeds into further acquisitions

- Selling the company itself (share sale) rather than the underlying property — though this carries its own complexities and is typically only viable for larger portfolios

- Using company structures for intergenerational wealth transfer, where shares can be gifted or transferred under inheritance tax planning arrangements

However, for investors intending to realise gains personally within a defined time horizon, the company structure can introduce additional tax layers that significantly erode the net return.

Corporate structures implicitly encourage longer holding periods. Because extracting sale proceeds is tax inefficient, many investors retain capital within the company and redeploy it into additional acquisitions. This creates a compounding effect where the corporate wrapper becomes a vehicle for portfolio expansion rather than a temporary tax shelter. The tax friction on extraction effectively locks capital into the property investment cycle, which can be advantageous for portfolio builders but problematic for investors who may need liquidity.

The Future of Corporate Ownership in the PRS

Despite the complexities, the trend toward corporate ownership is unlikely to reverse. Several structural forces support the shift, and the infrastructure supporting company-held property — from specialist lenders to accountancy firms — continues to mature.

Institutionalisation of the rental sector

Larger investors increasingly operate through corporate vehicles as a governance requirement rather than a tax choice. Build-to-rent operators, pension fund allocators, and family offices investing in residential property universally use corporate structures because they provide the legal and accounting framework expected by institutional stakeholders.

Financing evolution

Specialist lenders are expanding corporate mortgage products, and competition has made some SPV borrowing propositions more attractive than they were historically. But pricing remains lender- and case-specific, particularly across different LTVs, borrower profiles, and portfolio sizes.

Regulatory complexity

The expanding regulatory environment for landlords — including energy performance requirements, the Renters' Rights Bill, and local licensing schemes — favours investors who operate property as a business rather than holding it as a passive asset. Company structures, with their inherent requirement for structured record-keeping and compliance systems, are better suited to this environment.

These trends point toward a more professionalised landlord ecosystem, where ownership structures increasingly resemble small operating companies rather than passive asset holding. Limited companies are becoming an increasingly common vehicle for portfolio investment — not because of a single tax advantage, but because they can provide an operational and financial framework that suits leveraged, growth-oriented portfolios.

Investor Decision Framework

The key question investors should ask is not:

"Is a limited company tax efficient?"

The correct framework is:

1. What is the leverage profile of the portfolio? High leverage magnifies the Section 24 disadvantage under personal ownership and strengthens the case for incorporation.

2. Will profits be reinvested or extracted? Companies are most advantageous when profits are retained and compounded. If regular income extraction is required, the dividend tax layer erodes the benefit.

3. How large will the portfolio become? The fixed compliance costs of a company are better absorbed across a larger portfolio. Below a threshold of approximately three to four leveraged properties, the overhead may not be justified.

4. How important is refinancing flexibility? For portfolio landlords facing complex refinancing events, company structures can simplify lender underwriting and broaden the available product range.

5. What is the long-term exit strategy? If the investor intends to sell properties and extract proceeds, the double taxation on exit must be modelled. If the portfolio is intended as a long-term or intergenerational holding, the deferral benefit of corporate retention is more compelling.

The optimal structure emerges from these answers — not from a generic tax comparison.

Ownership structure should follow portfolio strategy

Investor Decision Checklist

Before choosing a structure, investors should evaluate several structural questions:

Leverage assessment

- What is the current loan-to-value ratio across the portfolio?

- How sensitive is cashflow to mortgage interest restrictions?

- Would full interest deductibility materially improve net returns?

Profit utilisation strategy

- Will rental profits be reinvested into further acquisitions?

- Is regular income extraction required for living expenses?

- Can profits be retained for 3-5 years without withdrawal?

Portfolio scale planning

- How many properties are planned over the next 5 years?

- Will the portfolio exceed 4 mortgaged properties (PRA threshold)?

- Can fixed compliance costs (£1,000-£2,500/year) be absorbed efficiently?

Refinancing considerations

- Are multiple refinancing events anticipated?

- Would SPV lending criteria simplify underwriting?

- Is access to specialist lenders important for portfolio growth?

Exit strategy clarity

- Is capital intended to be extracted or reinvested long-term?

- Are properties likely to be sold within 10 years?

- Is intergenerational wealth transfer a consideration?

These questions illustrate why the ownership structure decision should be treated as a strategic portfolio design choice rather than a purely tax-driven optimisation.

FAQ: Limited Companies for Property Investment

Do limited companies eliminate tax on rental income?

No. They change the timing and location of taxation. Companies pay corporation tax on rental profits (currently 19–25%), and shareholders pay dividend tax (8.75–39.35%) when profits are extracted. The combined burden can approach or exceed the personal income tax rate, particularly for investors who extract profits regularly.

Is it worth moving existing property into a limited company?

In many cases, the transfer costs make retrospective restructuring uneconomic. A transfer into a company can trigger CGT on market-value disposal principles and can also create SDLT for the acquiring company. Reliefs may exist in some qualifying business or partnership scenarios, but these are highly technical and should be verified before any restructuring is assumed to work.

Do limited companies avoid Section 24?

Yes. Section 24 of the Finance Act 2015 applies only to individual landlords. Limited companies can deduct mortgage interest in full when calculating taxable profits, which is the primary tax advantage driving incorporation for leveraged investors.

Can you refinance more easily through a company?

For portfolio landlords, company structures can simplify refinancing. Specialist SPV lenders often place more emphasis on portfolio rental coverage and cashflow than on personal income alone. However, company borrowing is not automatically cheaper, and pricing varies materially by lender and structure. The refinancing advantage is most pronounced for investors holding four or more mortgaged properties, where personal underwriting becomes more complex under the PRA's portfolio landlord rules.

What tax do you pay when selling property in a company?

The company pays corporation tax on the capital gain (19–25%). If the post-tax proceeds are then distributed to shareholders as dividends, a further layer of dividend tax applies.

Do lenders prefer company borrowers?

Not universally. Specialist SPV lenders have developed products specifically for company borrowers, and underwriting for portfolio landlords can be simpler through a corporate structure. However, mainstream lenders may still offer better rates for personal borrowers, and some lenders do not lend to companies at all. The lender landscape is segmented, and the optimal approach depends on portfolio size and structure.

What does it cost to run a property company each year?

Annual running costs typically include accountancy fees, Companies House filing fees, corporation tax return preparation, bookkeeping support, and potentially registered office services. For a small portfolio, these costs can represent a material percentage of net profit. For a larger portfolio, they are proportionally less significant and may be outweighed by the tax and structural advantages.

Final Investor Takeaway

Limited companies are not a universal optimisation strategy. They are a structural framework for running property portfolios as businesses.

For leveraged investors pursuing portfolio growth, they can materially improve cashflow, financing flexibility, and capital reinvestment. The restoration of full mortgage interest deductibility, the ability to retain and compound profits at the corporation tax rate, and the alignment with specialist lender underwriting criteria make the company structure a natural fit for scaling portfolios.

For smaller investors focused on income, the additional complexity, compliance cost, and layered taxation — particularly the dividend tax on extraction and the potential double taxation on exit — may provide little benefit and can actively reduce net returns.

The limited company structure represents the professionalisation of UK property investment rather than a tax optimisation strategy. As the private rented sector matures and regulatory complexity increases, corporate ownership provides the operational framework that modern property investment demands, transforming landlord activity from passive asset holding to active business management.

The correct ownership structure ultimately depends on how the investor intends to deploy, retain, and eventually realise capital — not simply on headline tax rates. The limited company decision is, at its core, a capital allocation decision. Investors who treat it as such are better positioned to make the choice that genuinely serves their long-term objectives.

Related PropMatch Analysis

-

Refinancing risk across the UK landlord sector: UK Buy-to-Let Refinancing Wave: Structural Risk Investors Are Underestimating

-

Capital gains tax mechanics investors often overlook: Capital Gains Tax on Property: What Actually Matters

-

Common property investment assumptions that fail in practice: Property Investment Pitfalls: Average Assumptions Failing UK Investors

Budget 2025 Hub: For comprehensive analysis of recent tax changes affecting property investors, visit our Budget 2025 Resource Center.

Sources and Verification Notes

- HMRC guidance on the finance cost restriction for residential landlords

- GOV.UK guidance on Corporation Tax rates

- GOV.UK guidance on dividend tax and the dividend allowance

- GOV.UK guidance on Capital Gains Tax rates for residential property

- GOV.UK guidance on Incorporation Relief

- Bank of England / PRA buy-to-let underwriting expectations, including the portfolio landlord definition

- Hamptons research using Companies House records on buy-to-let company incorporations — external market analysis rather than an official government statistical release

Stay Updated

Subscribe to our weekly briefings for curated property news and insights